Strategies & Capabilities

Active Quantitative Equity (AQE)

Human led, research tested: Only our best investment ideas survive the rigor of our analysis.

AQE Strategies

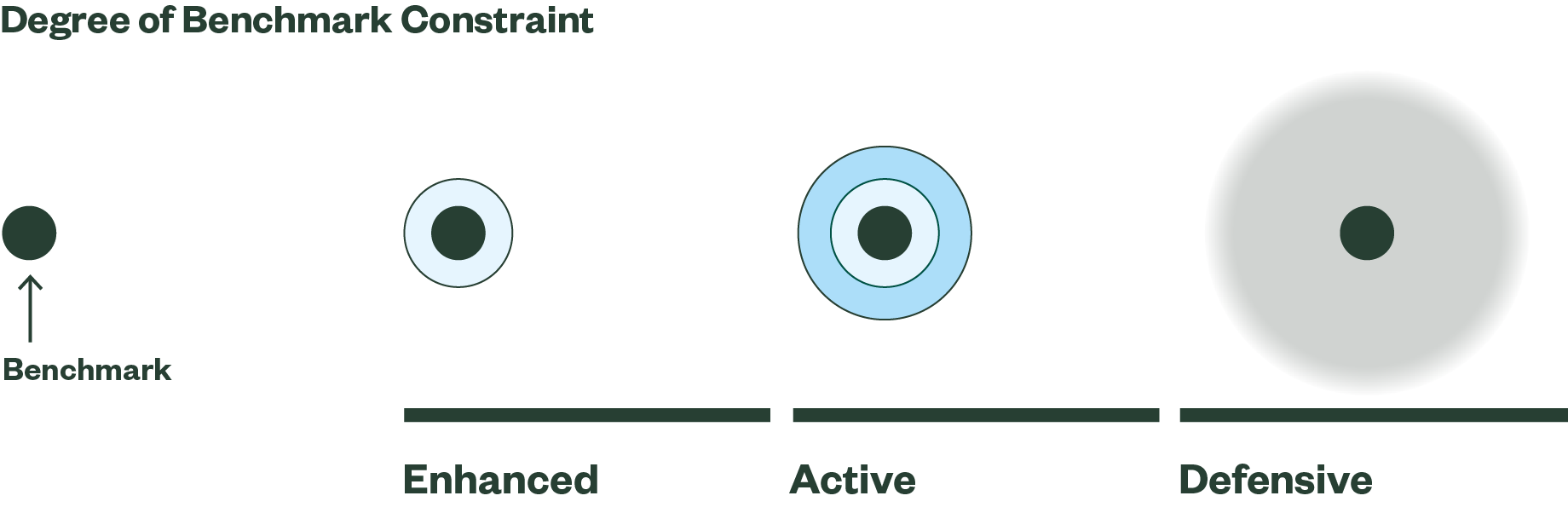

How can our capabilities help solve your investment problems?

How We Work

We are active managers, focused on solving investment problems. Built by a team with decades of experience, the stock-selection model that informs all of our solutions contains our best investment insights — carefully scrutinized, extensively tested and grounded in a strong economic rationale.

Our Latest Thinking

Meet The Team

Contact Us

For more than 30 years, research and innovation have been at the core of our efforts to deliver outperformance for our clients. Contact your State Street Global Advisors relationship manager, or email us to learn how to invest in AQE.